I generally divide my credit card perks into two categories: annual statement credits or lounge access that I actively try and use to enhance my travel experience, and travel insurance and purchase protection, which I hope to never need but appreciate being able to count on when I do.

But if you have a credit card as an authorized user, are you covered by an issuer’s travel insurance policy?

Benefits to authorized users

There are plenty of good reasons to add someone as an authorized user to your card, including sharing benefits with them, such as travel credits or other monthly statement credits like the $7 Dunkin’ credit (up to $84 per calendar year; enrollment is required and terms apply) on the American Express? Gold Card.

Authorized users also earn points on their spending and even?help your family members build credit, though remember that you’ll ultimately be responsible for any purchases they make on the card.

Many cards?allow you to add authorized users for free, but premium cards often charge a fee. For example, the?Chase Sapphire Reserve? charges?$75 per year to add an authorized user.

Authorized users and travel insurance

Understanding the terms of your insurance coverage before you need to use it so you don’t make any hasty and expensive mistakes based on incomplete information. As a reminder, the Chase Sapphire Reserve offers the following travel insurance benefits:

- Trip cancellation/trip interruption insurance

- Trip delay reimbursement

- Baggage delay insurance

- Lost luggage reimbursement

Related:?The best credit cards with travel insurance

The exact coverage requirements differ slightly for each policy, but taking trip cancellation and interruption insurance as an example, Chase lists those covered as ‘Covered Travelers’ to a domestic partner and family members, according to the terms and conditions.

Furthermore, to be covered by the card’s insurance, you must charge all or a portion of the trip cost to your card or have used Chase Ultimate Rewards points. Covered Travelers do not need to be traveling with the cardholder for benefits to apply.

There’s no differentiation between primary cardholders and authorized users, so I called Chase and spoke to a benefits administrator to confirm. The good news is that not only are authorized users covered, but in this case, their immediate family members would be as well. “Cardholder” doesn’t just mean the primary account holder — it means any user whose name is embossed on the Chase Sapphire Reserve credit card.

For trip delay reimbursement, the coverage of family, which includes domestic partners, is similarly defined as above:

To be eligible for this trip delay reimbursement coverage, all or a portion of your trip must’ve been booked using your Chase Sapphire Reserve card, including travel booked using Chase Ultimate Rewards points.

Related: The 7 credit cards with the greatest value for authorized users

Bottom line

Some people balk at paying the $75 a year fee to add authorized users to the Chase Sapphire Reserve, but when you consider that they earn full travel insurance coverage as if they were the primary cardholders, this becomes a much better value proposition. This benefit has saved me hundreds of dollars over the years, and Chase is known to offer some of the most comprehensive and generous coverage in the industry on its Chase Sapphire Preferred? Card and Sapphire Reserve card.

]]>If you earn a lot of credit card rewards, you may wonder if you’ll need to pay taxes on them. In most cases, no — your rewards aren’t considered taxable income.

That said, we’ve seen reports of people receiving 1099s for some sign-up bonuses. Specifically, many Chase cardholders have received 1099s for sign-up bonuses on Marriott cobranded cards, the Amazon gift card they received as the sign-up bonus on Amazon cards and for promos or credits they have received through their credit card, as first reported by FlyerTalk and Doctor of Credit.

I feel their pain. I’ve received two 1099’s from Chase in the past — one I was expecting and one I wasn’t.

So, let’s break down when you should expect a 1099 for your credit card rewards and what to do if you believe you received one in error.

Are credit card rewards taxable?

Generally speaking, credit card rewards are not taxable. In most cases, when you have to spend to earn rewards, those rewards are not considered taxable income. This means standard welcome bonuses, rewards you earn on your everyday credit card spending and credit card perks like statement credits are usually safe.

The exception to this rule is any bonus you get that doesn’t require spending, including referral bonuses and automatic bonuses for opening a new bank account. Since you don’t have to spend to earn them, these types of bonuses are considered taxable income.

Related: Should I pay my taxes with a credit card?

Which credit card rewards are taxable?

While most rewards aren’t taxable, one type is: referral bonuses you receive when someone applies for a credit card through your referral link. The bonus is considered income since you don’t have to spend to get these rewards. (Your friend, conversely, wouldn’t need to pay taxes on the bonus they earn for completing that spending.)

Related: Earn points, miles and cash back while doing your taxes

Is cash back taxable?

No, in most cases. A 2010 memorandum from the IRS says cash back earned via credit card spending is not considered taxable income. However, if you receive it as part of opening a bank account where you didn’t have to complete a minimum spending requirement, you must report it as income.

Related: The best cash-back credit cards

Are business credit card rewards taxable?

Just like with personal cards, welcome bonuses and the rewards you earn from making purchases on your business credit card are not considered taxable income. However, when claiming business expenses, you can only claim the net cost of an item after any statement credits you receive as a perk from your credit card rather than the full cost before the credits are applied.

Related: The best business credit cards

Are bank account sign-up bonuses taxable?

Yes. Bank account sign-up bonuses are similar to credit card referral bonuses — you don’t have to spend to earn them. This means they’re taxable, according to the IRS. Just like with credit card referral bonuses, there’s no guarantee you’ll get a 1099 for these bonuses, but you’re expected to claim them as income regardless.

Will I receive a 1099 for my credit card rewards?

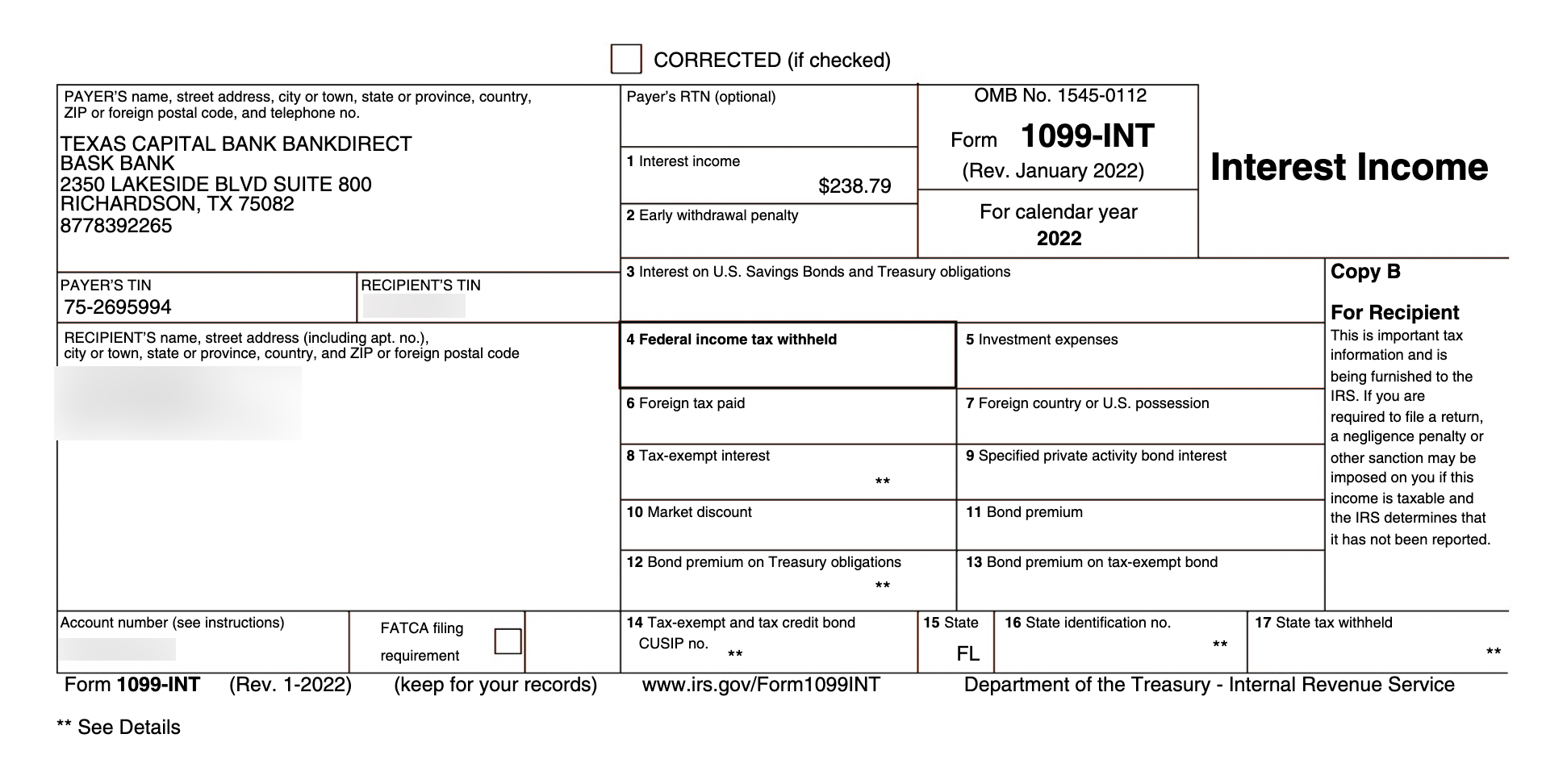

Sometimes, you’ll receive a 1099-MISC or a 1099-INT if a card has given you taxable rewards. A 1099 is often called an information return document for the IRS that shows the income you’ve received from a third party.

However, not all issuers will send these forms. We recommend keeping your own records since you’ll still need to report all of your income — even if you don’t receive a 1099.

Related: If I cash out my points and miles, do I have to claim it on my taxes?

Which issuers send 1099 forms for credit card rewards?

Most major issuers send 1099s for referral bonuses worth $600 or more. If you don’t get a 1099, you can request one from your bank or estimate the income. Even if the bank doesn’t send one, you must still report the income to the IRS.

Despite the general rule that you’ll only get a 1099 for referral bonuses, Capital One has also sent them in recent years for statement credits. They appear to be treating these as gifts, which can be taxable.

Additionally, in 2024, some have reported getting a 1099 from Chase for the Amazon gift card they received as a sign-up bonus on Amazon cards. I got my card during October’s Prime Day and received a $150 gift card as my bonus.

Sure enough, I got a 1099 for the $150 in the mail and a 1099 for the Chase referral bonuses I got the previous year.

TPG contributing editor Matt Moffitt received a 1099 from Capital One for his referral bonuses from 2023. He received 100,000 Capital One miles for four referrals, which Capital One valued at 1 cent each. As a result, his 1099 was for $1,000 in taxable income.

Many also report receiving a 1099 for their Marriott bonus of five free nights, which we haven’t seen in the past.

You can contact the issuer for clarification or correction if you receive a 1099 that you believe was in error.

Historically, banks have treated statement credits and bonus points as rebates on spending, which the IRS does not view as taxable income. So far, we haven’t seen major issuers consistently make this move, but we’ll keep an eye on it. If sign-up bonuses and statement credits are regularly taxed, that will go into our evaluation of a card’s net value year over year.

Related: Capital One expands benefits it considers taxable

Where do I report my credit card rewards income on a 1099?

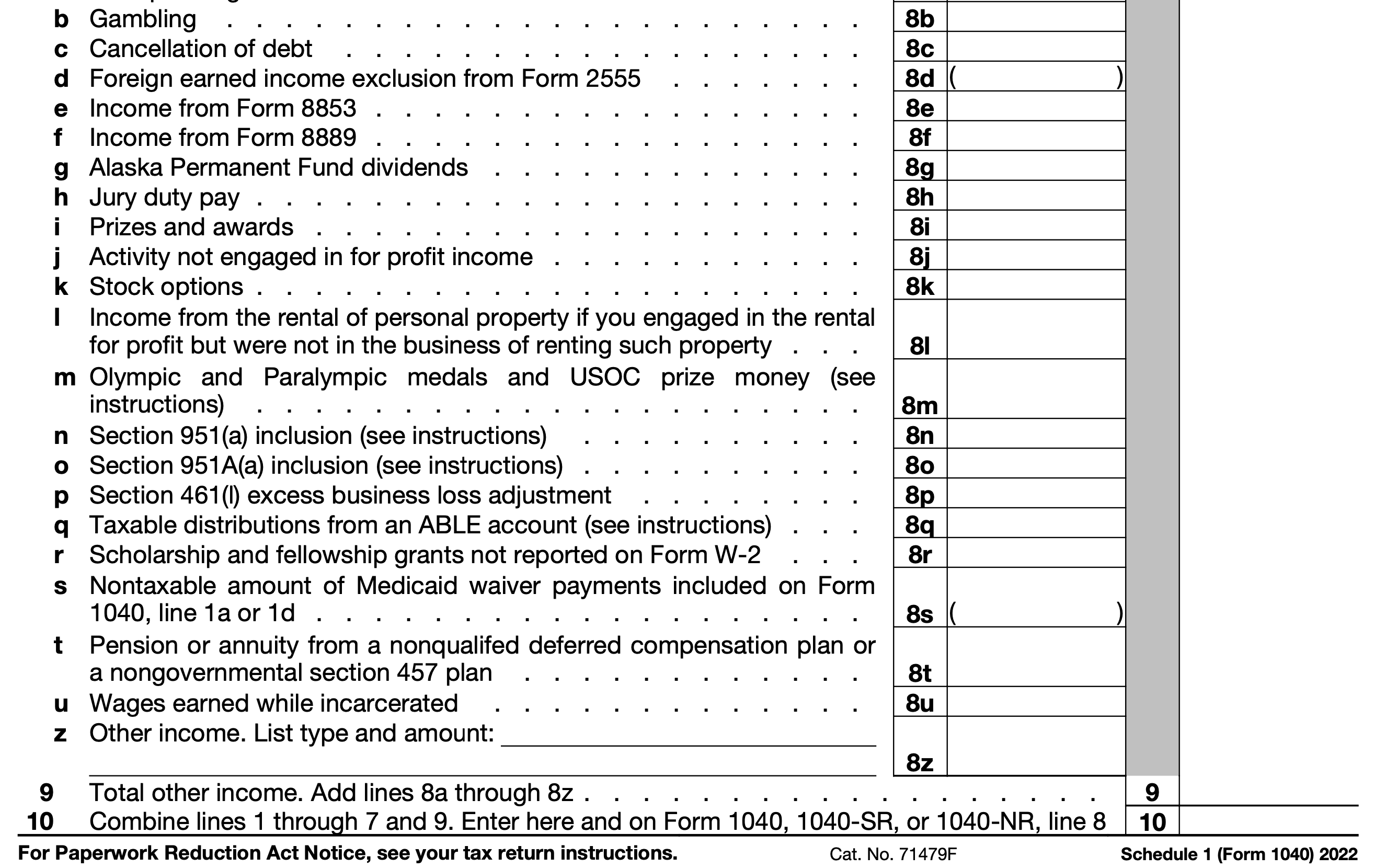

You should include the income under the heading “Other income” on line 8z of your 1040 as reported under the “Other income” from Schedule 1, line 22.

If you need to calculate the value of referral bonuses, use the issuer’s valuation of their points or miles versus a third-party valuation. For example, Capital One values their miles at one cent per point, whereas TPG’s February 2025 valuations peg them at 1.85 cents per point. When calculating the value of Capital One referrals, you’ll want to use their one-cent-per-point valuation.

Bottom line

Even if you’ve earned thousands of dollars worth of rewards this year through credit card welcome bonuses and everyday spending, you generally won’t have to pay taxes on those rewards. However, you must pay taxes on rewards from referral bonuses or opening a new bank account. Keep your own notes on these sources of income, as the bank may not send you a 1099 for these earnings.

If you’re concerned about owing taxes for your credit card rewards or you have further questions, consult a tax professional.

Related:? Earn points, miles and cash back while doing your taxes

]]>There are all sorts of travel credit cards (like hotel and?airline cards), and most fall into one of two categories — personal or business. Nearly anyone can apply for a personal credit card, but we often get one question: Do you need to own a business to get a business credit card?

A business credit card opens up a new set of possible welcome bonuses?and category bonuses. It’s also a great way to separate your business and personal expenses and give your small enterprise the spending power it needs to grow.

Here’s how you can qualify for one of your own.

Related: Business cards vs. personal cards

Do I need a business to get a business credit card?

To answer the question: Yes, you need a business to open a business credit card. But it’s important to define what exactly is a “business.” The qualifications for what qualifies as a business may differ?from what you might expect.

Do you sell items on Amazon, eBay or Craigslist? Do you teach music or sports? Ever act as a freelance writer or photographer? If you sell any goods or services, that could qualify you as a business owner.

But if you’re in one of these businesses, how do you explain that on a credit card application? You don’t have to have a registered business like an LLC or a corporation to apply. When applying for a business credit card, a section will ask what kind of business you own and request your business tax identification number. If you’re just in business on your own, you can choose to answer that you’re a sole proprietor, and in most cases, you can enter your Social Security number as your tax ID number.

Banks sometimes ask for supporting documentation to prove that you have a small business or earn income outside of an employer. So, you must tell the truth when applying for a business card.

Applying for a business card will also result in a hard pull on your credit report, and banks will look at your personal credit score when considering you for a business card. But once you have a business card, that line of credit will be separate from your personal one, so actions on a business account generally won’t affect your personal score (unless you default on payments, of course).

Related: What is a business credit card?

Bottom line

While you need a business to open a business credit card, something as simple as a side gig can qualify you for one. If you’re considering applying for a business credit card, look at our list of the best business credit cards. As always, it’s important to consider several factors when applying for cards. Do your due diligence and research before applying for a credit card.

]]>You may know that you can receive elite hotel status by holding the right cobranded credit card. Enroll in complimentary Marriott Bonvoy status as a perk of the following cards (terms apply):

- Silver Elite status:?Marriott Bonvoy Bold? Credit Card?and?Marriott Bonvoy Boundless? Credit Card

- Gold Elite Status:?Marriott Bonvoy Bevy? American Express? Card,?Marriott Bonvoy Business? American Express? Card,?The Platinum Card? from American Express?and?The Business Platinum Card? from American Express

- Platinum Elite status:?Marriott Bonvoy Brilliant? American Express? Card

You can also upgrade to Marriott Gold Elite status by spending $35,000 on purchases each calendar year on the Marriott Bonvoy Boundless Credit Card.

Related: Marriott elite status: What it is and how to earn it

Some cards also provide a certain number of elite night credits each year you hold the card, which can help you move up to a higher status.

As a reminder, you need to earn the following number of elite nights for status in the Marriott Bonvoy program:

- Silver Elite: 10 elite night credits per calendar year

- Gold Elite: 25 elite night credits per calendar year

- Platinum Elite: 50 elite night credits per calendar year

- Titanium Elite: 75 elite night credits per calendar year

- Ambassador Elite: 100 elite night credits per calendar year and at least $23,000 in qualified spending per calendar year

You will receive five elite night credits per calendar year on the Bonvoy Bold and 15 on the Bonvoy Boundless, Bonvoy Bevy and Bonvoy Business. Meanwhile, the Bonvoy Brilliant card offers an impressive 25 elite nights.

One elite night credit is also added to your account for every $5,000 you spend with the Marriott Bonvoy Boundless Credit Card.

You may not know that you can stack the complimentary elite nights if you hold more than one of these cards. Bonvoy does adopt a rule that you can only stack the nights from one personal card and one business card, so the magic formula to maximize your elite nights is to hold both the Marriott Bonvoy Brilliant American Express Card and the Marriott Bonvoy Business American Express Card to receive a total of 40 Bonvoy elite nights each calendar year.

You would already receive complimentary Platinum Elite status from the Bonvoy Brilliant card plus 40 elite night credits toward the 75 needed to achieve Titanium Elite.

Stacking these offers also counts toward your lifetime status goals and is a great shortcut toward earning elite status even if you aren’t staying at Marriott properties regularly.

]]>You may hope to earn elite status for the first time this year or you may be chasing a higher status tier. If you’re in that boat, you might plan to get there through organic travel or even a last-minute mattress run.

It’s often much easier to qualify for elite status with hotels than with airlines because award stays at major chains count toward hotel elite status.

However, if you risk falling a night short of earning status in 2024, do hotel stays from Dec. 31 to Jan. 1 count toward earning status this year or next? TPG reader Hailey asks:

After accounting for all my work travel I’m going to be one night short of Marriott Platinum status this year. If I book an award stay over New Year’s Eve, would that count towards this year (when I check in) or next year (when I check out)?

Related: Last-minute tips for locking in hotel elite status before the end of the year

Earning elite credits on New Year’s Eve stays

The short answer is that Marriott Bonvoy and?IHG One Rewards credit stays from Dec. 31 to Jan. 1 to the previous year, while Hilton Honors and World of Hyatt credit the stays to the following year.

That means if Hailey books a one-night stay over New Year’s Eve, it will push her over the threshold to earn Marriott Bonvoy Platinum elite status in 2024 to enjoy in 2025.

Things start to get a little more confusing if Hailey were to book a longer stay — for example, checking in Dec. 31 and checking out Jan. 3. Marriott and IHG split the stay, so nights up to (and including) Dec. 31 count toward the previous year while nights from Jan. 1 onward count toward the next year.

Hilton and Hyatt differ; the stay is not split, and the entire stay counts toward 2025.

A Hyatt agent has previously advised TPG that while the default setting is for all nights to post to 2025, members can call in and request a manual adjustment.? The booking can be split, so nights up to Dec. 31 count toward the 2024 World of Hyatt status requirements.

However, several TPG readers reported earlier this year that Hyatt refused to do this upon request by phone, so just to be safe, you may wish to ensure you reach the required number of nights by Dec. 31.

How to earn elite hotel status with a credit card

With the right credit card, you won’t need to worry about squeezing in a hotel stay on New Year’s Eve to earn elite status in your favorite hotel loyalty program.

The Marriott Bonvoy Brilliant? American Express? Card provides Platinum Elite status for all cardmembers. Alternatively, the Marriott Bonvoy Boundless? Credit Card?and?Marriott Bonvoy Business? American Express? Card each offer 15 elite night credits each year. And if you have both, those credits stack, meaning you’ll receive 30 elite night credits, more than half of the number needed for Bonvoy Platinum status.

If you have the World of Hyatt Credit Card, you’ll automatically get five tier-qualifying nights yearly. You’ll also earn two tier-qualifying nights for every $5,000 spent on your World of Hyatt Credit Card. The World of Hyatt Business Credit Card?provides five tier-qualifying nights for every $10,000 spent on the card each calendar year.

If you prefer Hilton Honors, the Hilton Honors American Express Aspire Card offers Diamond status.

The information for the Hilton Honors Aspire Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

IHG Platinum Elite status is offered as a perk of the IHG One Rewards Premier Credit Card?and?IHG?One Rewards Premier Business Credit Card.

If you hold the United Club? Infinite Card, you can also?register for complimentary IHG Platinum Elite status.

Finally, you can enjoy Gold status with both Marriott Bonvoy and Hilton Honors with The Platinum Card? from American Express (enrollment is required).

Bottom line

It’s risky to leave requalifying for status until the very last day possible, especially given the big gap in benefits across hotel status tiers.

That being said, Hailey will be able to earn her last elite qualifying night Dec. 31, even if her stay stretches into January of the following year.

If you plan on using New Year’s travel to qualify for hotel elite status, monitor your account during the first week of January to ensure your stay credits as you expect it to.

]]>When you share your points and miles redemptions with your friends and family, they’ll likely ask for your advice on which credit card they should get next. If they take your advice, you may be able to benefit by sending them your referral link and earning a bonus.

But what if your friend or family member wants a business card, and you only have personal cards?

Great news: You may still be able to refer them. However, since each issuer has its own way of rewarding referrals, a few different factors will determine whether you’ll be able to earn a bonus.

Here’s what you need to know about earning referral bonuses on both personal and business credit cards.

American Express

American Express is the most versatile issuer for earning referral bonuses from different cards. You can earn a referral bonus when someone gets a business card from your personal referral link or vice versa.

However, you and the person you’re referring need to take a few steps to get the referral bonus with a different card.

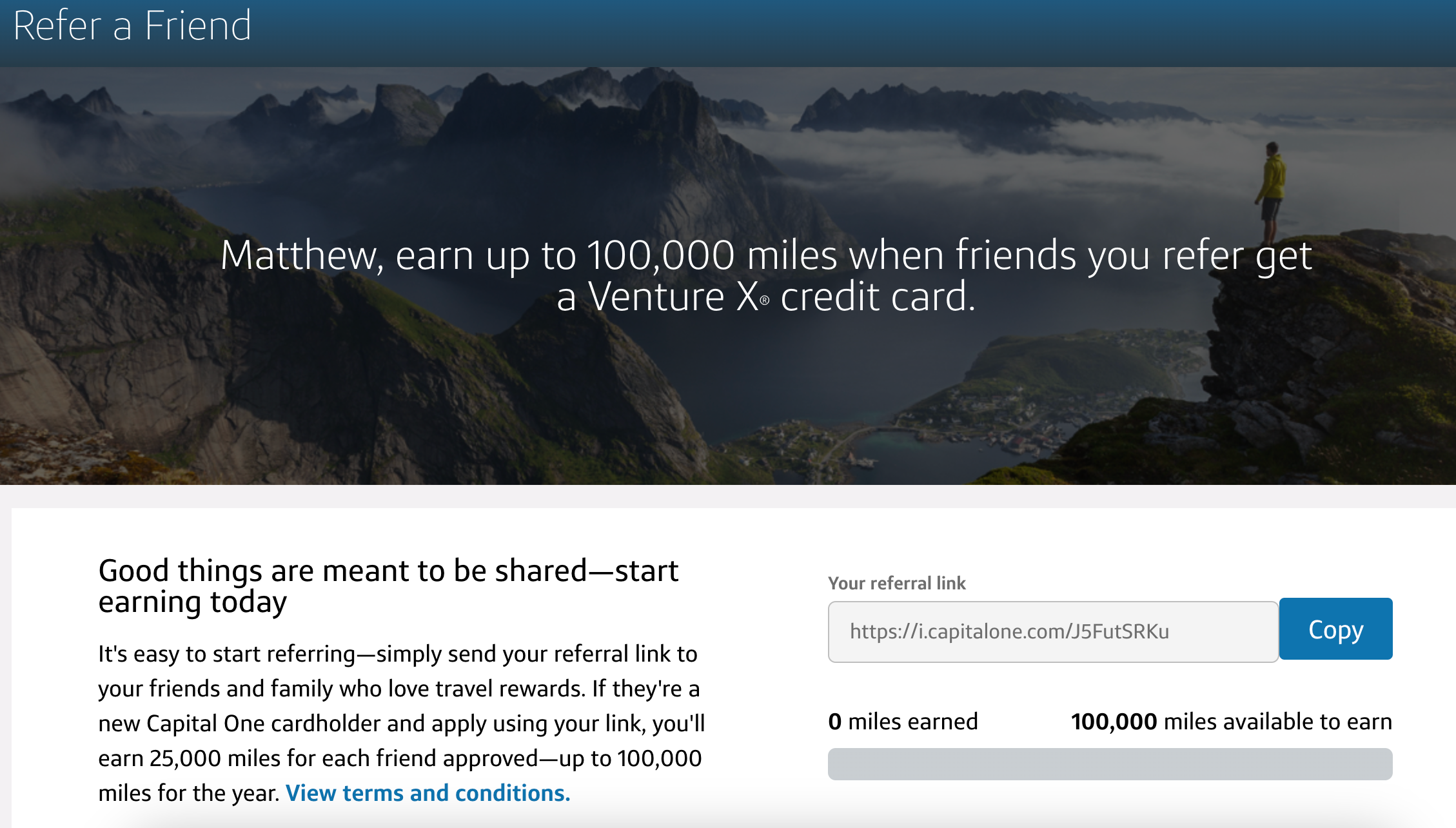

First, log into your Amex account, click “Rewards & Benefits” from the menu in the top left-hand corner, then select “Refer a Friend.”

You can send an email directly to your friend or family member or copy and paste a referral link. Then, when your recipient opens the link, the pop-up window will indicate the card you used to refer them.

For example, I could create a referral link for my Hilton Honors American Express Aspire Card. My friend would see the option to apply for any of the three Hilton Honors personal cards.

They could click “Business Cards” on the left-hand side to see a referral offer for the business version.

For cobranded cards like the Hilton ones, you can generally only refer within that card family.

However, when I referred my friend using my American Express? Gold Card link, they had cobranded cards, cash-back and Membership Rewards cards to choose from. If you have a card that earns Membership Rewards points, using its referral link will likely give your friend or family member the most card options.

The information for the Hilton Aspire Amex card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

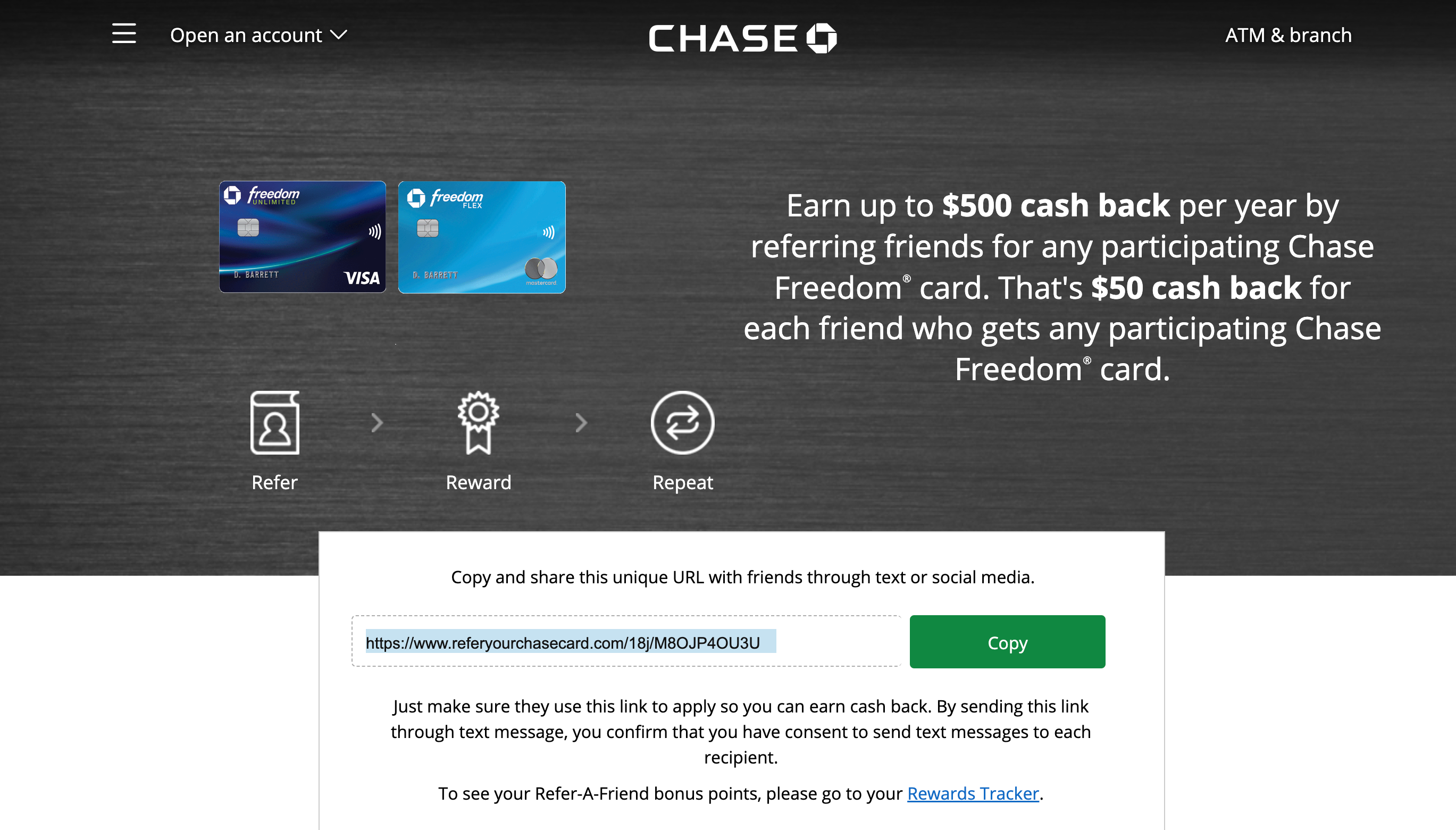

Chase

Generally, Chase only lets you earn a referral bonus when you refer someone to a card within the same family as the one you have.

For example, if you have the Chase Freedom Flex?, you can refer someone for the Chase Freedom Unlimited?.?You need to be an Ink cardholder to refer someone for one of the?Ink Business cards.

If you have a personal cobranded card, like the IHG One?Rewards Traveler Credit Card, you can refer someone to get any card within that family. In this case, you can refer someone to the IHG One?Rewards Premier Business Credit Card even if you only have a personal IHG card.

Related: The best Chase credit cards

Capital One

Capital One referral bonuses are more limited. They’re targeted instead of widely available, so you’ll need to check your account to see if you have a referral link you can send to a friend. If you have a link, your friend will need to navigate through it to see which cards are available to them on your referral.

The consistent limitation for Capital One referrals is that personal credit card holders will only be able to refer personal cards. You must have a Capital One business account to refer someone to a Capital One business card.

Related: Capital One Refer a Friend: What you need to know about this generous program

Citi

Citi is far more stingy with its referral offers than the other issuers listed here. It offers referral bonuses, but they’re specifically targeted. So, you’re far from guaranteed to earn a referral bonus if you have a friend who wants a Citi card.

Bottom line

Referring friends or family members to one of your favorite credit cards is a great way to share the world of points and miles. Earning a referral bonus makes sharing that knowledge even sweeter.

Check your referral links before your friend or loved one applies for a new card. If you can share one, it’s a win for you both.

Related: Refer businesses to Capital One and earn up to $1,500 per referral

]]>One of the best problems in the points world is figuring out which credit card bonus category will give you the most bang for your buck on a certain purchase.

When dining at a hotel, this can be especially tricky — should you use a card that earns bonus points on dining or hotel purchases?

Let’s jump into questions that can guide you on which card you should use when dining at a hotel.

How does the eatery code?

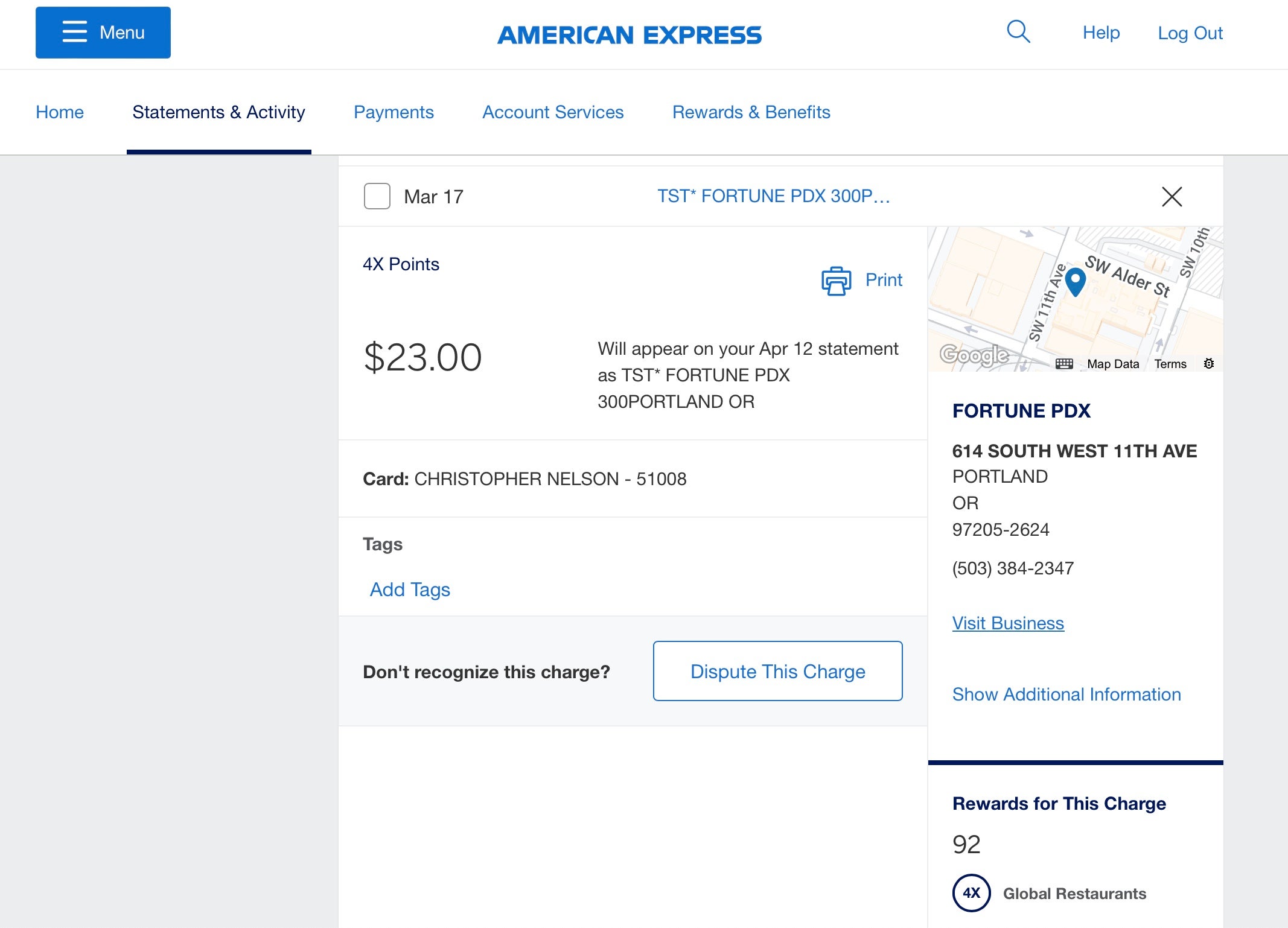

Bars and restaurants at hotels can be tricky because sometimes they code as hotel or travel purchases and sometimes as dining. For most issuers, if a restaurant or bar is located inside another business, such as a hotel, it will code as a hotel or travel purchase.

However, I recently popped into a bar attached to a hotel I was not staying at. I used my American Express? Gold Card and it coded as dining at a restaurant, so I earned 4 points per dollar spent (on up to $50,000 in purchases per calendar year, then 1 point per dollar).

So, each restaurant or bar attached to a hotel can code differently on a case-by-case basis. I have noticed that if the restaurant or bar is a chain, it tends to code as dining.

If you’re unsure how the eatery will code, a safe bet is to use a card that earns bonus points on both dining and hotel purchases, such as the Chase Sapphire Preferred? Card or Chase Sapphire Reserve?.

Note that the Sapphire Reserve will not earn bonus rewards on travel purchases until after the first $300 is spent on travel annually.

Related: The best credit cards for dining

Are you staying at the hotel?

If you are staying at the hotel and don’t want to take a chance on how the restaurant will code, your best option is to charge your meal to your room. Then, your restaurant or bar bill will be added to your overall hotel bill, ensuring that it will be coded as a hotel expense.

If you have a card that earns bonus rewards on travel but not dining, like the Ink Business Preferred? Credit Card, this is a good way to make sure you’ll earn bonus rewards on your dining purchase.

And if you have a cobranded credit card with the hotel, you’ll earn bonus points on the purchase and may even tap into additional perks like a dining discount.

While spending on cobranded credit cards doesn’t always make sense, one of the best reasons to do so is to rack up large bonus multipliers on hotel stays.

Related: How to choose a hotel credit card

Should I use my dining card or my hotel’s cobranded credit card?

If you have a card with great earning rates on dining at restaurants, like the Amex Gold Card (on up to $50,000 per year, then the base rate of 1 point per dollar), it can be tempting to use it to pay at your hotel restaurant and earn valuable transferable rewards rather than hotel points.

However, most cobranded cards have outstanding earning rates for purchases at their hotels, so you’ll almost always come out ahead by charging the meal to your room and paying with your cobranded hotel card when you can.

For instance, if you take a chance that the restaurant will code as dining and use your Amex Gold to pay your bill, you stand to earn 4 points per dollar on that purchase (on up to $50,000 in purchases per calendar year, then 1 point per dollar) — an 8% return, according to TPG’s November 2024 valuations.

But if you take that chance and the purchase codes as a hotel instead of a restaurant, you’ll only earn 1 point per dollar.

If, however, you charge the bill to your room and pay with your cobranded hotel card, you’ll ensure that you get your card’s bonus-earning hotel rate for the purchase.

Related: Marriott Bonvoy Boundless credit card review: Worth keeping year after year

Understanding bonus multipliers

If you’re a hotel elite and staying at the property you’re dining at (as opposed to just popping in for drinks), you’ll earn elite bonus points on your entire folio in addition to the points from your credit card spending, giving you even more reason to charge your dining bill to your room.

For Marriott, that breaks down as follows:

- General members: 10 points per dollar

- Silver: 11 points per dollar

- Gold: 12.5 points per dollar

- Platinum: 15 points per dollar

- Titanium and Ambassador: 17.5 points per dollar

And since most cobranded hotel cards include a level of elite status, you’re almost always better off charging your meal to your room and using your hotel card to pay the full folio at the end of your stay.

For instance, the Marriott Bonvoy Brilliant? American Express? Card comes with automatic Platinum Elite status. If you charge your meal to your room and pay for your stay with your Brilliant card, you’ll get a total of 21 points per dollar — 15 for your elite status and 6 for paying with your Brilliant.

According to TPG’s November 2024 valuations, those 21 points per dollar equate to over a 17% return — much higher than even the best dining card in your wallet.

The bonus multiplier structure is similar for chains such as IHG, Hilton and Hyatt. The higher your status, the more bonus points you will earn.

Related: Comparing the best hotel elite status tiers and how to earn them

Bottom line

When dining at a hotel you aren’t staying at, your safest option is to use a card that earns bonus rewards on both dining and travel purchases, so you get a great earning rate regardless of how the bill codes. But if you’re staying at the hotel, you’ll likely want to charge the bill to your room and use a cobranded hotel card or other card that earns bonus rewards on travel purchases.

Don’t leave valuable rewards on the table — make sure you pull the right card out of your wallet every time you dine at a hotel restaurant or bar.

Related: Best hotel credit cards of 2024

]]>Having access to expedited-security programs like?Global Entry and?TSA PreCheck?can be extremely valuable if you travel frequently. Even better, although?these programs carry fees, there are a number of credit cards that reimburse you for them.

Those credits might seem redundant if you’ve already enrolled or have more than one available. Fortunately, you can still put any extra credits you have to use.

How can I use my Global Entry credit on someone else?

When you pay for a Global Entry or TSA PreCheck application using an eligible card like the Capital One Venture Rewards Credit Card or Chase Sapphire Reserve?, all the card issuer sees is a charge from U.S. Customs and Border Protection. They won’t be able to tell whose name is on the application, so the statement credit should be issued automatically within a few days (assuming you haven’t already used it). Even if the name on the application was apparent, it might not matter since the terms and conditions don’t limit the fee credit to the cardholder.

If you’ve already used your own credit, you may still be able to help?someone else enroll by making?them an authorized user on your account. The Platinum Card? from American Express allows you to add up to three authorized users for $195 apiece per year (see rates and fees), and each authorized user gets their own $120 application credit for Global Entry. If you know a few people who want to sign up for expedited security, you can essentially get it for them at a discount, along with other benefits like lounge access and hotel elite?status. Not all cards extend the statement?credit to authorized users, so make sure yours is eligible before adding cardholders?to your account.

TSA PreCheck is another program that makes it quicker and easier to go through airport security (passengers don’t have to take off belts and shoes?or remove laptops and toiletries from their bags). Cards that include Global Entry credits can also cover just the cost of TSA PreCheck if you don’t want to wait for up-to-12-month?processing times for Global Entry approval.

Global Entry speeds up reentry into the U.S. after an international flight. TSA PreCheck is included with Global Entry and the price difference is minimal ($78-$85 depending on where you enroll versus $120). Both programs are valid for five years.

Related:?Why you should get TSA PreCheck and Clear — and how you can save on both

Bottom line

Before you give away a spare application fee?credit, make sure you don’t need it yourself. Global Entry membership lasts for five years, but you could end up wanting to reapply sooner. Many application centers are backlogged, and getting an appointment can take a while; it makes sense to renew your membership early so it doesn’t lapse while you’re waiting for an interview.

Related: What is Clear airport security — and is it worth it?

For rates and fees of the Amex Platinum card, click here.

]]>Here’s something you might have been wondering: What happens when a payment that gets refunded was one you used to help you earn a credit card welcome bonus? That’s an excellent question that one of our readers, Stephanie, asked us about:

“I recently got the [Hilton Honors American Express Aspire Card] and had to spend $4k in order to receive the 150,000 bonus Hilton Honors points.* I spent well over $4k on the card in the first month alone on flights, rental cars and hotels for a trip I had coming up in November. The entire trip ended up getting canceled … and almost all of the spend I had generated was refunded back to me. However, I had already been awarded the Hilton bonus points and they were in my Hilton account. My question is: Was this just a fluke? I have to imagine credit card companies usually take your points away and make you spend more…. If I already transferred the bonus from the card to a partner airline, would the card company then get the airline to send back the miles?”

The information for the Hilton Honors American Express Aspire Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

*This welcome offer is no longer available.

Related: How this reader visited 8 countries in 3 years using points and miles

Do refunds count against spending toward a Welcome bonus?

The good news is that, by and large, credit card issuers don’t typically rescind a welcome bonus after they’ve awarded it, no matter if the purchases being refunded were used to help meet a spending requirement. Unfortunately, American Express does have a different policy compared to most of the other major issuers.

I contacted the major U.S. issuers for their policies on the subject, and here’s what each said:

American Express

This particular reader question specifically asks about an American Express-issued Hilton credit card. Amex’s policy in their terms and conditions state that in the case of a refund, rewards will be rescinded.

Unfortunately, this extends to welcome bonuses as well. An Amex representative confirmed that if a refund is issued for purchases that helped you reach a welcome bonus spending threshold, that welcome bonus will be rescinded unless you meet the spending requirement through other purchases before the deadline.

Bank of America

Like most of the other issuers, Bank of America confirmed that you would not have your welcome bonus taken away if you received a refund for purchases that helped you attain the bonus.

Chase

Chase confirmed that it doesn’t rescind credit card welcome bonuses after they are awarded. So, if you complete the spending requirements, receive the bonus and then get a refund for purchases that may have helped you meet the requirements, you would still keep your bonus.

Capital One

We reached out to Capital One, but we did not receive confirmation about its policy regarding welcome bonuses in the case of refunds.

Citi

Citi confirmed that if you’ve met a spending requirement and received your points before a refund hits your account you would keep your welcome bonus.

However, the representative I talked with did point out that refunds made before you received your bonus would be recognized as deductions against the minimum spending target. Customers would have to make up that spend in order to earn the welcome bonus.

Warning: Don’t abuse these policies

While this is great to hear (except for Amex), ensure that you aren’t abusing these policies. Issuers will flag you for suspicious behavior, such as applying for a card, making large purchases to earn a welcome bonus and then turning them in for a refund after you receive your bonus. Chase is especially known for shutting down accounts with little warning when it suspects foul play.

If it’s a random and understandable occurrence, you should have little to worry about. But don’t use these policies to cheat the system — you’re risking a shutdown and encouraging issuers to adopt stricter policies, which hurts everyone.

Bottom line

Airline cancellations can happen, leading to refunds, confusion and all sorts of headaches. The good news is that, for the most part, your welcome bonus should be safe if you receive a refund after you’ve met the minimum spend requirement for a welcome bonus, with the exception of American Express.

Related: Best credit card welcome offers

]]>When you first see it, the term “negative balance” can make you think you made a mistake, like forgetting to pay your credit card balance. However, a negative balance on your credit card is actually a good thing because it means the bank owes you money instead of the other way around.

Still, you may be less than thrilled to have your money tied up in a credit card account. So, we’re breaking down the best things to do when you find yourself with a negative credit card balance. We’ll cover the different things you can do, all requiring varying degrees of effort on your part.

Why do I have a negative balance?

You’ll most often have a negative credit card balance after you’ve made a return or received a refund for something.

Recently, I experienced this when I made a return before paying the balance on my Citi? /? AAdvantage? Platinum Select? World Elite Mastercard? . However, the return wasn’t processed until after I had paid my bill. The result? A negative balance on my card of just more than $100.

The information for the Citi AAdvantage Platinum Select World Elite Mastercard has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

For something as minor as this, I’ll just use this card to spend around $100 to take care of my negative balance. However, if you have a much larger negative balance, such as after canceling a major trip, you may want to look into other options.

Related: Getting a refund after you cancel your credit card

Keep spending on the card

This is the simplest option. Just keep using the card with a negative balance, and the purchases you make on the card will eventually bring you back to zero or a positive balance. With this approach, there is almost never a need to contact the bank or do anything out of the ordinary.

Transfer the balance to another card on your account

If you have a balance on another card within the same account, you can contact the bank and ask to transfer your negative balance to a card on which you owe money. This approach takes a small amount of effort, but it gives you the benefit of putting your future spending on a card that will earn you the most points rather than just trying to use the negative balance on one specific card.

TPG credit cards managing editor Matt Moffitt recently had a negative balance of more than $400 on his Platinum Card? from American Express due to a refund. He also had a positive balance of around $500 on a Delta card. Instead of spending more on his Platinum Card, he used the American Express chat feature to ask an agent to transfer the negative balance and put it toward the Delta balance. The agent manually completed this action, and it took less than 48 hours for the balance to show up on the Delta card.

Related: The best way to pay your credit card bills

Ask for cash

If you have a significant negative balance and don’t need to transfer it to another card, you may want to ask to receive the negative balance in cash. Often, banks will give you the cash amount through direct deposit or mail you a physical check for the amount they owe you.

Again, this requires contacting the bank and possibly waiting for a check in the mail; however, it can be worth it to have the freedom to spend that money on a different card that will earn you more rewards than the card with the negative balance. Or, you may just want the cash flow.

Related: How 5 minutes of chat got me 85,000 points plus $150

Bottom line

A negative credit card balance is a good thing because it means the bank owes you money. When you find yourself with a negative balance, choose the option that works best for you to use that money and maximize your rewards.

The easiest way is to just spend on that particular card. However, you can also ask your bank to apply the balance to another card on your account or send you the cash by direct deposit or a check in the mail.

Related: Best travel credit cards

]]>